Loading

Bonanza Offer FLAT 20% off & $20 sign up bonus Order Now

International Financial Reporting Standards (IFRS) are established by the International Accounting Standards Board (IASB). These standards facilitate in communicating the financial results of a company to its stakeholders so that they can analyse the information and take appropriate decisions regarding entering into a financial transaction with it. These standards also facilitate in comparing the financial results of two and more companies that prepare their financial statements by complying with the IFRS (IFRS 2013).

The local Generally Accepted Accounting Principles (GAAP) is standards set by the local regulatory authority of that country, which is adopted by companies that are based in the concerned country. The selected country for this paper is the UK. This paper focuses on the difference between UK GAAP and IFRS. The three significant differences between UK GAAP and IFRS are illustrated by representing them in the form of financial statements. These differences are related to intangible assets, provisions and government grants. There will also be a discussion of problems faced by the entity in adoption of IFRS for the first time in a chosen country. Besides this, the impact of adoption of IFRS on the financial performance and position of a company is also discussed in this paper (Ernst & Young 2012).

There is an existence of significant differences between IFRS and UK GAAP. Under IFRS, the statement of changes in equity includes the statement of recognised gains and incomes. The cash flow statement includes both cash, as well as, cash equivalents and there is a classification of interest and dividends on the basis of their nature into three categories i.e. operating, investing and financing. Under certain circumstances, there is an involvement of bank overdraft in cash and cash equivalents. In contrast the UK GAAP states that there is a separate presentation of recognised gains and loses and changes in the shareholder’s fund. There is no consideration given to cash equivalents under these standards in the cash flow statement and there is also an inclusion of bank overdrafts in cash. The interest, dividends and taxes are classified into different categories of an item (KPMG 2003).

The cost of inventory is calculated by using LIFO method, whereas in UK GAAP, LIFO method is rarely used by companies for the evaluation of inventory in their financial statements. The cost of agricultural produce is recorded at cost or net realisable value, whichever is less, but in IFRS, the cost of agricultural produce is recorded at the value attained by subtracting point of sale cost from the fair value. Under IFRS, some of the equity shares are classified as liabilities. In addition to this, the dividend earned on these shares are treated as interest on the accrual basis in income statement, whereas there is a requirement to record all shares under shareholder’s funds and the shares that are owned by employees under ESOP scheme are treated as assets of a company under UK GAAP (World GAAP Info 2008).

In addition to this, the distribution of dividend is recognised in the year to which it relates. There is a requirement to differentiate the amount of dividend and shareholder’s fund with regard to the equity and non equity. The revaluation of financial statements under IFRS is done either on the mandatory basis or on the option basis. Despite this, the adjustments are made on the basis of current purchasing power if the currency of an enterprise is hyperinflationary. On the other hand, under UK GAAP, there is a rare possibility of revaluation of assets, except property; along with this, there is no additional requirement to be fulfilled by the company under the hyperinflationary nature of currency (Ernst & Young 2011).

Under IFRS, power to control is the foundation of consolidation and subsidiaries are treated as financial assets if they are excluded from the consolidation. The computation of minority interests is done either on the basis of carrying amounts of subsidiaries or on consolidation; while in UK GAAP, there is a requirement of consolidation only if dominant influence is exercised regardless of the existence of formal power. The treatment of subsidiaries is done as equity if these are excluded from consolidation and have a significant influence on the business of the company (World GAAP Info 2008). In addition to this, the evaluation of minority interest is done on the basis of carrying amounts on consolidation. Under IFRS, there is an exclusion of those acquired assets and liabilities, which do not adhere with the requirements of recognition under other standards. In addition to this, the income statement recognises negative goodwill. There is a capitalisation of transaction cost and the cost of acquisition includes expenses related to the registration and issue of equity securities. On the other hand, UK GAAP recognises those acquired assets and liabilities which do not meet the requirements of recognition under other standards. There is no capitalisation of transaction costs and it involves deduction of cost of issuing shares from gross proceeds and it has been credited to equity shareholder’s funds (KPMG 2003).

There is an exclusion of property under operating lease from investment property and it is recorded at the fair value along with changes in the income statement under IFRS. The dual use investment property is classified only if the separate parts can be sold separately. On the other hand, the investments held under operating leases are considered under investment property and only that part is classified under investment property which can be let out not necessarily to be disposed off separately under UK GAAP. Besides this, there is recognition of investment property at the open market value in the financial statements and the record of changes is to be treated under reserves in this system (World GAAP Info 2008).

The impairment is calculated annually for those tangible fixed assets that have a life span of 50 years and the monitoring of cash flows is to be done for five years after a value in use in UK GAAP, whereas impairment is not calculated annually for property, plant and equipment under IFRS and there is no requirement of monitoring after a specified time period. Under UK GAAP, there is an inclusion of provisions in financial statements regarding the sale and termination of an operation. This type of provision includes estimated operating losses for the future period. On the other hand, there is no requirement to make provisions for future operating losses under IFRS. Under UK GAAP, there is no deduction of government grants from the cost of fixed assets to which these grants relate, whereas government grants related to the fixed assets are deducted from the cost of that particular asset (KPMG 2003).

The main difference for the treatment of intangible assets between UK GAAP and IFRS is that the intangibles, such as development costs are capitalised and amortised under IFRS, but it is not either capitalised or amortised under UK GAAP. In the IFRS system, it is recorded only if there is a possibility of recovering of the deferred taxes, whereas under UK GAAP, the amount which is not likely to be recovered related to deferred tax assets is recorded. When deferred taxes are related to intra-group transactions, the tax rate of selling entity is applicable under UK GAAP while the tax rate of buying entity is applicable on the deferred taxes associated with the intra-group transactions in IFRS (Ernst & Young 2011).

There is an adjustment of goodwill only if the recovery of deferred tax assets exceeds the original estimate in IFRS. In addition to this, it is provided from the perspective of the re-evaluation of a financial statement of hyperinflationary subsidiaries; while there is no recognition of deferred taxes under these conditions, as well as, there is no recognition of adjustment of goodwill when the amount of acquisition of deferred tax assets exceeds the estimated value under UKGAAP. Under IFRS, deferred tax assets are not discounted, whereas in UK GAAP, deferred taxes can be discounted (World GAAP Info 2008).

Under IFRS, the profits and losses from the repurchase or settlement of debt are not considered as extraordinary items, whereas it is treated under interest in UK GAAP. There is a separate accounting standard for hedging under IFRS while no detailed information is provided under UK GAAP. The financial instruments that are not classified under derivatives can be used for hedging the exposure of risk related to currency fluctuations in IFRS but these instruments cannot be used for hedging the risk related to the foreign currency fluctuations under UK GAAP.

No mandatory format related to the income statement is given under IFRS but companies that follow UK GAAP have to present their income statement in a format given under these standards. The treatment of contingent assets and liabilities under UK GAAP guide that companies have to provide full information to stakeholders as per the rules and regulations of Companies Act 1985, even if this results in serious bias. On the other hand, only some information can be disclosed rather than full disclosure under IFRS. The recognition of unrealised profits in the income statement is allowed under IFRS, whereas it is allowed to recognise the unrealised profits in income statement under UK GAAP. There are no guidelines given for share based payments under IFRS, whereas expenses related to shares are recorded on the basis of intrinsic value under UK GAAP. Under UK GAAP, extra ordinary items are removed effectively and specific rules are mentioned under these standards for the treatment of these items. In contrast, IFRS do not provide any disclosure regarding extraordinary items and these are present in certain special circumstances.

There is a need to disclose detailed information related to the credit risk, currency risk, and interest rate risks before the effect of hedging under IFRS, whereas the information related to these risks is provided in the financial statements after the effect of hedging in case of UK GAAP.

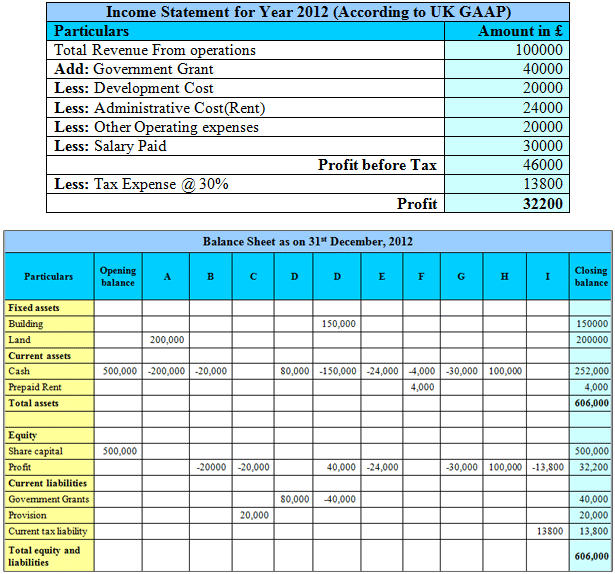

The PR Solutions was established in 2012. PR Solutions started its business with cash of £500000. The entity started its business in London and was setup to provide the consultancy service in the United Kingdom. PR Solutions follows the accounting standards of the United Kingdom (UK GAAP). Before starting the company, the promoters conducted some research and development for £50000.

Following are the some basic accounting treatment in the United Kingdom

Transactions in Year 2012

Transactions for Year 2013

| Income Statement for Year 2013 (According to UK GAAP) | |

| Particulars | Amount in £ |

| Total Revenue From operations | 180000 |

| Add: Government Grant | 40000 |

| Less: Administrative Cost(Rent) | 24000 |

| Less: Other Operating expenses ( provision) | 20000 |

| Less: Salary Paid | 50000 |

| Profit before Tax | 126000 |

| Less: Tax Expense @ 30% | 37800 |

| Profit | 88200 |

| Balance Sheet as on 31st December, 2013 | |||||||||||

| Particulars | Opening balance | A | B | C | D | E | F | G | H | J | Closing balance |

| Fixed assets | |||||||||||

| Building | 150,000 | 100,000 | 250,000 | ||||||||

| Land | 200,000 | 200,000 | |||||||||

| Current assets | |||||||||||

| Cash | 252,000 | -100,000 | -20,000 | -4,000 | -50,000 | 180,000 | -13,800 | 244,200 | |||

| Prepaid Rent | 4,000 | -4,000 | 4,000 | 4,000 | |||||||

| Total assets |

| 698,200 | |||||||||

| Equity | |||||||||||

| Share capital | 500,000 | 500,000 | |||||||||

| Profit | 32,200 | -20,000 | 40,000 | -24,000 | -50,000 | 180,000 | -37,800 | 120,400 | |||

| Current liabilities | |||||||||||

| Government Grants | 40,000 | -40,000 | 0 | ||||||||

| Provision | 20,000 | 20000 | 40,000 | ||||||||

| Current tax liability | 13,800 | 37,800 | -13,800 | 37,800 | |||||||

| Total equity and liabilities |

| 698200 | |||||||||

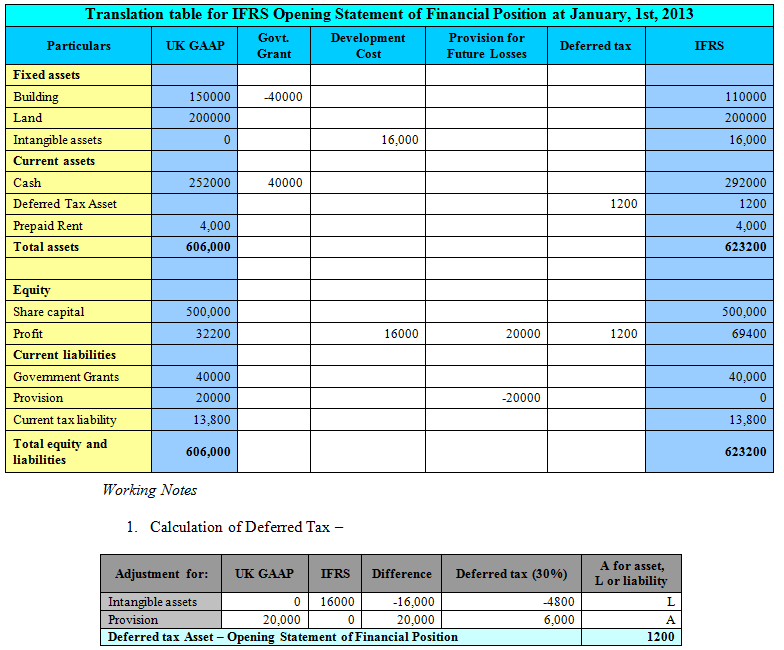

| Translation table for IFRS Opening Statement of Financial Position at December, 31st, 2013 | ||||||

| Particulars | UK GAAP | Govt. Grant | Development Cost | Provision for Future Losses | Deferred tax | IFRS |

| Fixed assets | ||||||

| Building | 250,000 | -40,000 | 210000 | |||

| Land | 200,000 | 200000 | ||||

| Intangible assets | 0 | 12,000 | 12000 | |||

| Current assets | ||||||

| Cash | 244,200 | 40,000 | 284200 | |||

| Deferred Tax Asset | 7200 | 7200 | ||||

| Prepaid Rent | 4,000 | 4,000 | ||||

| Total assets | 698,200 |

|

|

|

| 717400 |

| Equity | ||||||

| Share capital | 500,000 | 500,000 | ||||

| Profit | 120,400 | 12,000 | 40000 | 7200 | 179600 | |

| Current liabilities | ||||||

| Government Grants | 0 | 0 | ||||

| Provision | 40,000 | -40000 | 0 | |||

| Current tax liability | 37,800 | 37800 | ||||

| Total equity and liabilities | 698,200 | 717400 | ||||

Income statement – translation table

| Particulars | UK GAAP | Government Grant | Development Cost | Provision | Deferred tax | IFRS |

| Revenue | 180000 | 180000 | ||||

| Government Grant | 40000 | 0 | 40000 | |||

| Development Cost | 0 | 12000 | 12000 | |||

| Administrative Cost | -24000 | -24000 | ||||

| Provision | -20000 | 20000 | 0 | |||

| Salary Paid | -50000 | -50000 | ||||

| Tax Paid | -37800 | 7200 | -30600 | |||

| Profit | 88200 |

|

|

|

| 127400 |

Working Notes

| Adjustment for: | UK GAAP | IFRS | Difference | Deferred tax (30%) | A for asset, L or liability |

| Intangible assets | 0 | 12000 | -12000 | -3600 | L |

| Provision | 40000 | 0 | 40000 | 12000 | A |

| Deferred tax Asset – Opening Statement of Financial Position | 8400 | ||||

| Less: previously created | 1200 | ||||

| Total | 7200 | ||||

IFRS financial statements for Year 2013

| Statement of Financial Position at December, 31st | ||

| Particulars | 2012 | 2013 |

| Fixed assets | ||

| Building | 110000 | 210000 |

| Land | 200000 | 200000 |

| Intangible assets | 16,000 | 12000 |

| Current assets | ||

| Cash | 292000 | 284200 |

| Deferred Tax Asset | 1200 | 7200 |

| Prepaid Rent | 4,000 | 4,000 |

| Total assets | 623200 | 717400 |

| Equity | ||

| Share capital | 500,000 | 500,000 |

| Profit | 69400 | 179600 |

| Current liabilities | ||

| Government Grants | 40,000 | 0 |

| Provision | 0 | 0 |

| Current tax liability | 13,800 | 37800 |

| Total equity and liabilities | 623200 | 717400 |

| Statement of Comprehensive Income for 2013 | |

| Particulars | Amount |

| Revenue | 180000 |

| Government Grant | 40000 |

| Development Cost | 12000 |

| Administrative Cost | -24000 |

| Provision | 0 |

| Salary Paid | -50000 |

| Tax Paid | -30600 |

| Profit | 127400 |

| Statement of Changes in Equity for the year ended December, 31st, 2013 | |||

| Particulars | Share Capital | Profit | Total |

| Balance at Jan, 1, 2013 | 500,000 | 69,400 | 569,400 |

| Total Comprehensive Income for 2013 | 127,400 | 127,400 | |

| Balance at Dec, 31, 2013 | 500,000 | 196,800 | 696,800 |

| Cash Flow Statements for the year 2013 | |

| Particulars | Amount in € |

| Cash flow from operating activities |

|

| Profit before tax provision | 144,000 |

| Amortization of intangible asset | -4,000 |

| Cash generated (used) from operations | 140,000 |

| Working Capital changes | |

| Deferred Tax Assets | -6,000 |

| Government Grants | -40,000 |

| Income tax paid | -13,800 |

| Net cash from operating activities | 92,200 |

| Cash flow from investing activities | — |

| Investment in Building | -100,000 |

| Net cash from Investing activities | -100,000 |

|

| |

| Cash flow from financing activities | — |

|

|

|

| Net increase in cash and cash equivalents | -7,800 |

| Cash and cash equivalents at beginning of period | 292000 |

| Cash and cash equivalents at end of period | 284200 |

The impact of the first adoption of IFRS on the entity’s financial position and performance

| Opening Statement of Financial Position – reconciliation | ||||

| Particulars | UK GAAP | Note | Difference | IFRS |

| Fixed assets |

|

|

| |

| Building | 150,000 |

| 40000 | 110000 |

| Land | 200,000 | 200000 | ||

| Intangible assets | 0 | 2 | 16,000 | 16,000 |

| Current assets | ||||

| Cash | 252,000 | 40,000 | 292000 | |

| Deferred Tax Asset | 0 | 4 | 1,200 | 1200 |

| Prepaid Rent | 4,000 | 0 | 4,000 | |

| Total assets | 606,000 | 623,200 | ||

| Equity | ||||

| Share capital | 500,000 | 0 | 500,000 | |

| Profit | 32,200 | 3 | 37200 | 69,400 |

| Current liabilities | ||||

| Government Grants | 40,000 | 1 | 0 | 40,000 |

| Provision | 20,000 | 5 | 20000 | 0 |

| Current tax liability | 13,800 | 0 | 13,800 | |

| Total equity and liabilities | 606,000 | 623200 | ||

The first adoption of IFRS by PR Solutions has impacted its financial position in a significant manner due to the above differences in the accounting treatments under two different standards, namely IFRS and UK GAAP.

| Closing Statement of Financial Position – reconciliation | ||||

| Particulars | UK GAAP | Note | Difference | IFRS |

| Fixed assets |

|

|

| |

| Building | 250,000 | 1 | 40000 | 210000 |

| Land | 200,000 | 0 | 200000 | |

| Intangible assets | 0 | 2 | 16,000 | 12,000 |

| Current assets | ||||

| Cash | 244,200 | 40,000 | 284200 | |

| Deferred Tax Asset | 0 | 4 | 1,200 | 7200 |

| Prepaid Rent | 4,000 | 0 | 4,000 | |

| Total assets | 698,200 | 717,400 | ||

| Equity | ||||

| Share capital | 500,000 | 0 | 500,000 | |

| Profit | 120,400 | 59200 | 179,600 | |

| Current liabilities | ||||

| Provision | 40,000 | 3 | 20000 | 0 |

| Current tax liability | 37,800 | 0 | 37,800 | |

| Total equity and liabilities | 698200 | 717400 | ||

Entities based in the UK that have adopted UK GAAP face problems at the time of implementing IFRS for the first time for preparing its financial statements. In order to change the financial statements, as per the IFRS, entities have to do analysis of those items and activities that have an impact on their financial statements. Besides this, the collection of the data which is required to make changes in the existing figures due to the changes in the procedure of accounting treatment of different items is also done by the entity. The company have to reassess the accounting policies and standards as these have a great influence on the format of financial statements. It is a very long process and requires huge amount of cost and time. Businesses also face issues related to the audit procedure of the financial position as there is a requirement to audit the financial statements fully from UK GAAP to IFRS (KPMG 2013).

There is a requirement to do detailed analysis of adjustments as IFRS requires inclusion of additional adjustments related to different items that are included in the statements. The adoption of IFRS requires disclosing more information as compared to UK GAAP. Company also finds difficulty in engaging with Audit Committees before a prescribed time so as to spread awareness among them about the procedure, as well as, the impact of adoption of IFRS (KPMG 2013).

At the time of adoption of IFRS for first time, company has to follow a set of procedure issued by the IASB, if these entities are adopting it after 1 January 2009 (Deloitte 2013). The treatment of deferred tax is an additional requirement under IFRS that makes the process complex and difficult. The adoption of IFRS forces entity to prepare financial statements of the year in which it is adopted, in addition to a year prior to the adopted year. It also faces difficulty with regard to treatment of taxes. This is because taxes greatly influence the amount of profit earned by the company. The company, in order to reduce its tax liabilities so as to reduce the negative impact on its profitability, has to adopt different measures (Moore Stephens). Besides this, a firm has to classify its assets and liabilities as per the accounting standards of IFRS due to the absence of recognition of some assets and liabilities under UK GAAP. There is also a need to reclassify the opening balances of assets and liabilities of a firm as per the guidelines of IFRS (Deloitte 2013).

References

Deloitte. 2013. IFRS 1 — First-time Adoption of International Financial Reporting Standards. [Ernst & Young. 2011. UK GAAP vs. IFRS. [Online]. Available at: Ernst & Young. 2012. International GAAP 2012 - Generally Accepted Accounting Practice Under International Financial Reporting Standards. John Wiley & Sons

IFRS. 2013. About us. KPMG. 2003. IAS compared with US GAAP and UK GAAP. KPMG. 2013. IFRS Practice Issues. World GAAP Info. 2008. UK FRS.

Upload your Assignment and improve Your Grade

Boost Grades